Computes a heteroskedasticity-consistent covariance matrix estimator for an

ordinary least squares model fitted with stats::lm(). The function returns

a rich S3 object that stores the covariance matrix, HC weights, leverage

values, method parameters, and model metadata.

Arguments

- object

An ordinary least squares model fitted by

stats::lm().- type

A character string specifying the HC estimator. The default is

"hcbeta".- ...

Method-specific constants. Unknown names are rejected. See Details for the accepted names, defaults, and parameter domains.

Value

An object of class hcinfer_vcov. The covariance matrix is stored in

object$vcov and is returned directly by vcov().

Details

For a linear model with design matrix \(X\), OLS residuals \(\hat e_t\), and HC weights \(g_t\), the estimator is

$$\widehat{\Psi}_{HC} = (X'X)^{-1} X' \widehat{\Omega} X (X'X)^{-1},$$

where \(\widehat{\Omega} = diag(\hat e_t^2 g_t)\). The supported

estimators are "hc0", "hc1", "hc2", "hc3", "hc4", "hc4m",

"hc5", "hc5m", and "hcbeta".

Additional arguments in ... are method-specific. The defaults are:

"hc0","hc1","hc2","hc3","hc4", and"hc4m": no method-specific arguments."hc5":k = 0.7."hc5m":k = 0.7,k1 = 1,k2 = 0,k3 = 1,gamma1 = 1, andgamma2 = 1.5."hcbeta":c1 = 7,c2 = 0.75,lower = 0.01,upper = 0.99,a_max = 10000, andb_max = 10000.

For "hc5" and "hc5m", k, k1, k2, and k3 must be nonnegative,

while gamma1 and gamma2 must be positive. For "hcbeta", c1 must be

nonnegative, c2 must be positive, and lower and upper must lie in

(0, 1) with lower < upper. The HCbeta truncation is

\(w_t = max(lower, min(1 - h_t, upper))\).

Both a_max and b_max must be finite and lie in [50, 25000]; they cap

the shrunk Beta shape parameters \(\tilde a\) and \(\tilde b\) and

default to 10000. The two caps can be set independently through ... for

sensitivity analysis. HCbeta remains defined when \(h_t = 1\) because it

truncates \(1 - h_t\) before evaluating the Beta CDF. In contrast, HC2

through HC5m require a strictly positive leverage complement.

References

White, H. (1980). A heteroskedasticity-consistent covariance matrix estimator and a direct test for heteroskedasticity. Econometrica, 48(4), 817-838. doi:10.2307/1912934

Hinkley, D. V. (1977). Jackknifing in unbalanced situations. Technometrics, 19(3), 285-292. doi:10.1080/00401706.1977.10489550

MacKinnon, J. G. and White, H. (1985). Some heteroskedasticity-consistent covariance matrix estimators with improved finite sample properties. Journal of Econometrics, 29(3), 305-325. doi:10.1016/0304-4076(85)90158-7

Davidson, R. and MacKinnon, J. G. (1993). Estimation and Inference in Econometrics. Oxford University Press.

Cribari-Neto, F. (2004). Asymptotic inference under heteroskedasticity of unknown form. Computational Statistics and Data Analysis, 45(2), 215-233. doi:10.1016/S0167-9473(02)00366-3

Cribari-Neto, F. and da Silva, W. B. (2011). A new heteroskedasticity consistent covariance matrix estimator for the linear regression model. AStA Advances in Statistical Analysis, 95(2), 129-146. doi:10.1007/s10182-010-0141-2

Cribari-Neto, F., Souza, T. C., and Vasconcellos, K. L. P. (2007). Inference under heteroskedasticity and leveraged data. Communications in Statistics - Theory and Methods, 36(10), 1877-1888. doi:10.1080/03610920601126589

Li, S., Zhang, N., Zhang, X., and Wang, G. (2016). A new heteroskedasticity-consistent covariance matrix estimator and inference under heteroskedasticity. Journal of Statistical Computation and Simulation, 87(1), 198-210. doi:10.1080/00949655.2016.1198906

Examples

schools <- PublicSchools |>

dplyr::mutate(

income_scaled = income / 10000,

income_scaled_sq = income_scaled^2

)

fit <- lm(expenditure ~ income_scaled + income_scaled_sq, data = schools)

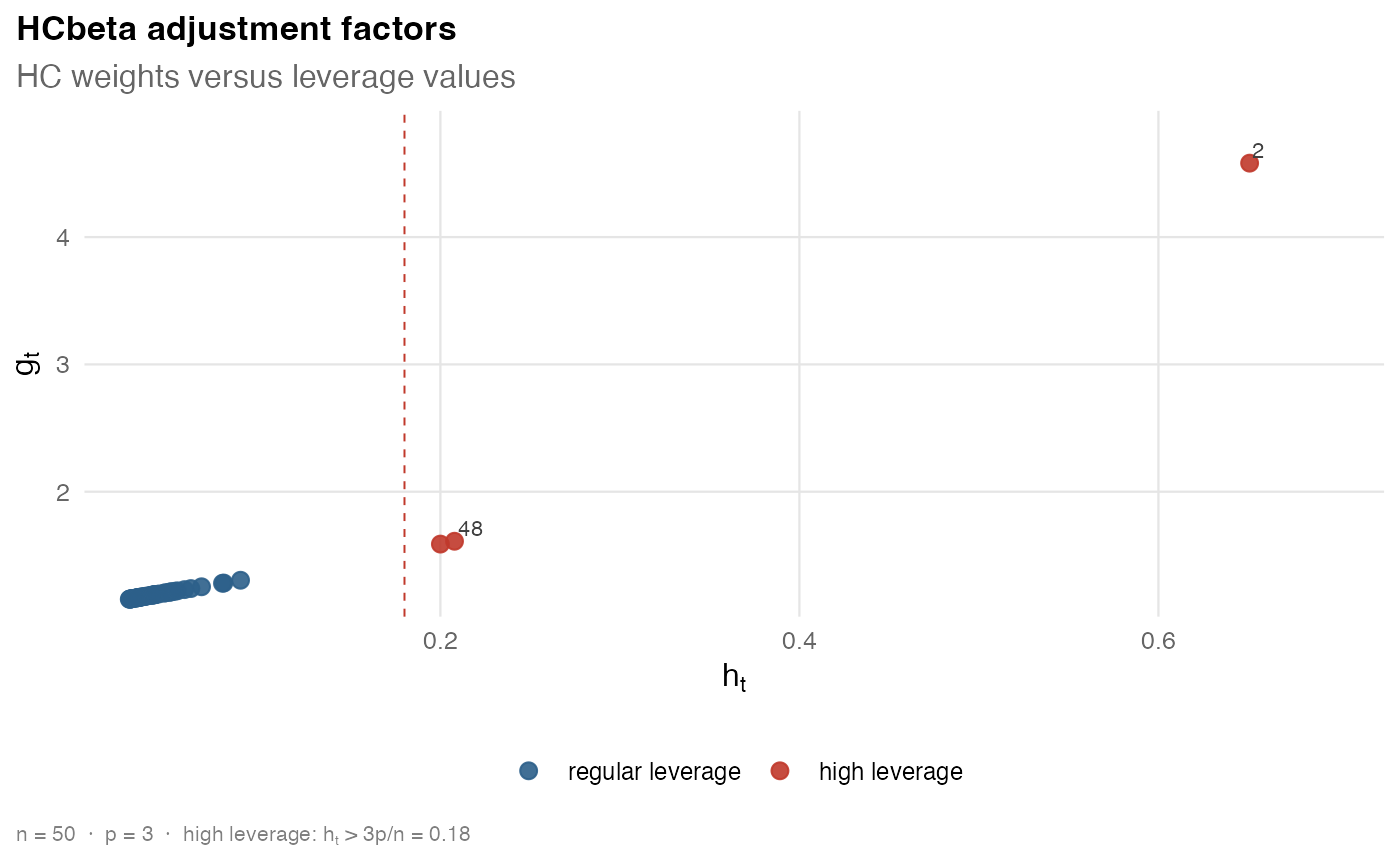

cov <- vcov_hc(fit, type = "hcbeta")

cov

#>

#> ── 🥪 HCbeta robust covariance ─────────────────────────────────────────────────

#> 📐 Model: `expenditure ~ income_scaled + income_scaled_sq`

#> Dimension: 3 x 3

#> Observations: 50

#> Parameters: 3

#> 🎯 Maximum leverage: 0.6508

#> ⚖️ Maximum robust weight: 4.5807

#> Use `vcov()` to extract the stored covariance matrix.

vcov(cov)

#> (Intercept) income_scaled income_scaled_sq

#> (Intercept) 723617.6 -1962262 1312195

#> income_scaled -1962262.2 5329884 -3569755

#> income_scaled_sq 1312195.3 -3569755 2394627

plot(cov)

# Sensitivity analysis with nondefault HCbeta caps

vcov_hc(fit, type = "hcbeta", a_max = 20000, b_max = 20000)

#>

#> ── 🥪 HCbeta robust covariance ─────────────────────────────────────────────────

#> 📐 Model: `expenditure ~ income_scaled + income_scaled_sq`

#> Dimension: 3 x 3

#> Observations: 50

#> Parameters: 3

#> 🎯 Maximum leverage: 0.6508

#> ⚖️ Maximum robust weight: 4.5807

#> Use `vcov()` to extract the stored covariance matrix.

vcov_hc(fit, type = "hc5", k = 0.7)

#>

#> ── 🥪 HC5 robust covariance ────────────────────────────────────────────────────

#> 📐 Model: `expenditure ~ income_scaled + income_scaled_sq`

#> Dimension: 3 x 3

#> Observations: 50

#> Parameters: 3

#> 🎯 Maximum leverage: 0.6508

#> ⚖️ Maximum robust weight: 2946.7866

#> Use `vcov()` to extract the stored covariance matrix.

vcov_hc(fit, type = "hc5m", k = 0.7, k1 = 1, k2 = 0, k3 = 1)

#>

#> ── 🥪 HC5m robust covariance ───────────────────────────────────────────────────

#> 📐 Model: `expenditure ~ income_scaled + income_scaled_sq`

#> Dimension: 3 x 3

#> Observations: 50

#> Parameters: 3

#> 🎯 Maximum leverage: 0.6508

#> ⚖️ Maximum robust weight: 8438.7828

#> Use `vcov()` to extract the stored covariance matrix.

# Sensitivity analysis with nondefault HCbeta caps

vcov_hc(fit, type = "hcbeta", a_max = 20000, b_max = 20000)

#>

#> ── 🥪 HCbeta robust covariance ─────────────────────────────────────────────────

#> 📐 Model: `expenditure ~ income_scaled + income_scaled_sq`

#> Dimension: 3 x 3

#> Observations: 50

#> Parameters: 3

#> 🎯 Maximum leverage: 0.6508

#> ⚖️ Maximum robust weight: 4.5807

#> Use `vcov()` to extract the stored covariance matrix.

vcov_hc(fit, type = "hc5", k = 0.7)

#>

#> ── 🥪 HC5 robust covariance ────────────────────────────────────────────────────

#> 📐 Model: `expenditure ~ income_scaled + income_scaled_sq`

#> Dimension: 3 x 3

#> Observations: 50

#> Parameters: 3

#> 🎯 Maximum leverage: 0.6508

#> ⚖️ Maximum robust weight: 2946.7866

#> Use `vcov()` to extract the stored covariance matrix.

vcov_hc(fit, type = "hc5m", k = 0.7, k1 = 1, k2 = 0, k3 = 1)

#>

#> ── 🥪 HC5m robust covariance ───────────────────────────────────────────────────

#> 📐 Model: `expenditure ~ income_scaled + income_scaled_sq`

#> Dimension: 3 x 3

#> Observations: 50

#> Parameters: 3

#> 🎯 Maximum leverage: 0.6508

#> ⚖️ Maximum robust weight: 8438.7828

#> Use `vcov()` to extract the stored covariance matrix.